US manufacturing beef imports remain robust

Key points

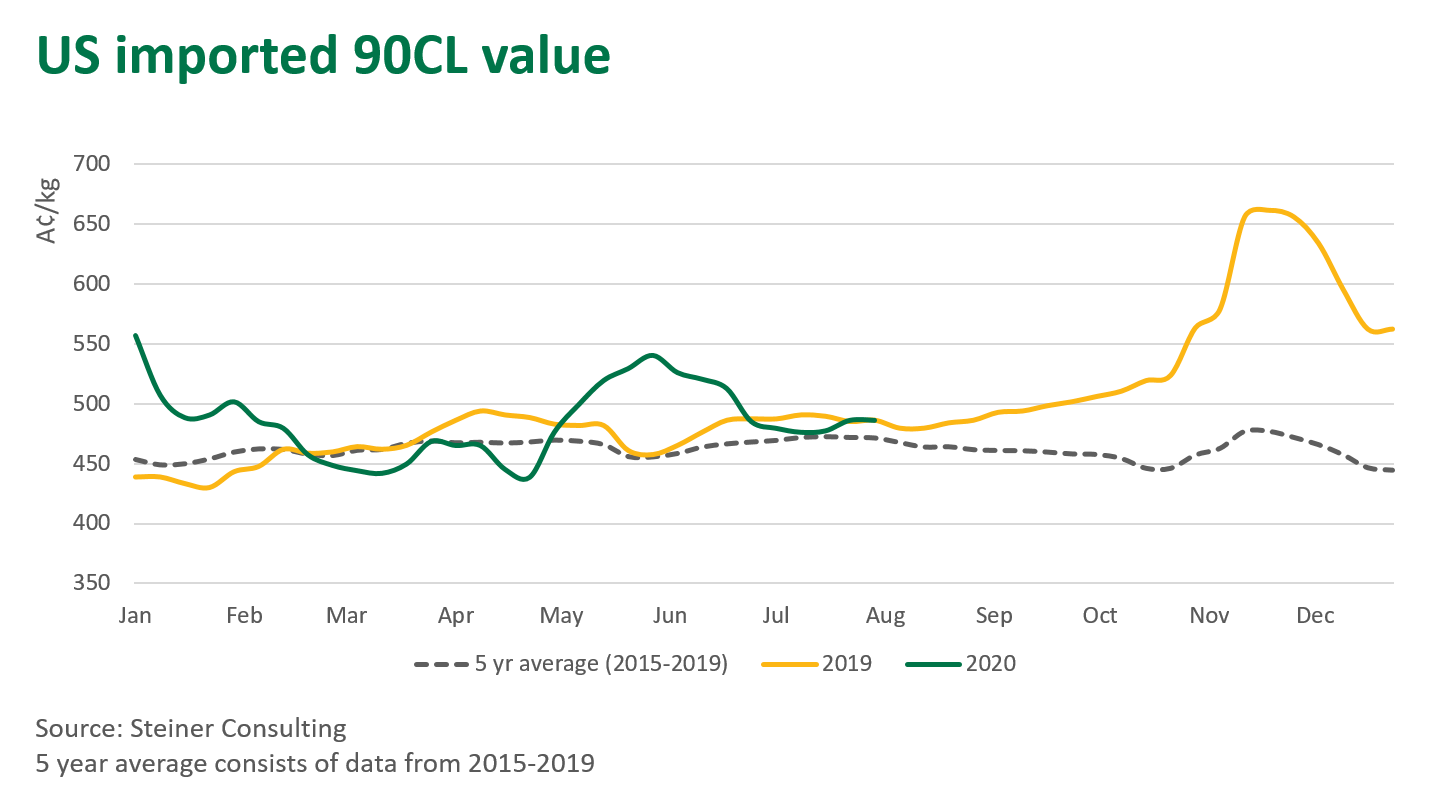

- Imported 90CL prices remain above the five-year average

- The Australian dollar continues to gain momentum lifting to US72¢

- Competitor presence within US beef market has been growing, led by Mexico

The US imported 90CL (Chemical Lean) indicator (a benchmark price for manufacturing beef into the US) is holding steady above the 2015-2019 average. However, market conditions across the US remain unsettled, with COVID-19 demand uncertainty, seasonally low Oceania offerings, shifting exchange rates and the increasing presence of South American suppliers all currently troubling factors.

Steiner Consulting reported that the imported beef market steadied last week after some previous uncertainty and volatility. The imported 90CL beef indicator was unchanged this week at US220¢/lb CIF (AUD486¢/kg CIF).

Tightening beef supply from Australia and New Zealand has provided some support to US import prices, while uncertainty regarding the demand outlook has also been a contributing factor. Surges in COVID-19 cases has forced California to shut down indoor dining at restaurants, bars and movie theatres. There is also the possibility of roll backs in other key states. Fortunately, demand through retail channels remains upbeat.

The Australian dollar has seesawed in 2020, largely against the US dollar, as volatility in global markets has affected investor sentiment. Since plummeting in March amid heightened global uncertainty, the Australian dollar has rallied, and is now back above year-ago levels, reaching 72US¢ on Tuesday. As a result, product from lower cost competitors in Southern and Central America has contributed towards more competitive market conditions on the back of an appreciating Australia dollar.

For the year-to-date, total US beef imports are up 8% on 2019 levels, as strong prices for lean grinding beef have undoubtedly caught the attention of international suppliers. Mexico has emerged as a key supplier to the US, with an abundance of local beef, strong US retail demand and the soft value of the Peso all supporting Mexican packers. For the year-to-date, US imports from Mexico have just tipped past 160,000 tonnes swt, and are second only to Canada, where volumes are just shy of 175,000 swt for the same period.

Recent outputs from South American suppliers have been growing, with Brazil, Argentina and Nicaragua beef exports benefiting from a more competitive price point due to soft currency values. COVID-19 related trade barriers have slowed some South American beef exports to China, which has resulted in these suppliers looking to diversify exports to other markets such as the US.

For more information on the US market, see the weekly report produced by Steiner Consulting.

© Meat & Livestock Australia Limited, 2020