US sheep industry contracts

Recent USDA data demonstrates a sustained decline in the US sheep industry, with imported lamb the major beneficiary.

Domestic industry update

Recent USDA data shows a continued downward trend in the US sheep industry, with the US flock estimated to be 5.23 million head on 1 January 2019. The figure is down 0.7% on the previous year and the lowest total on record.

The estimated number of replacement lambs also fell, underpinning the expectation for further contraction again in 2019.

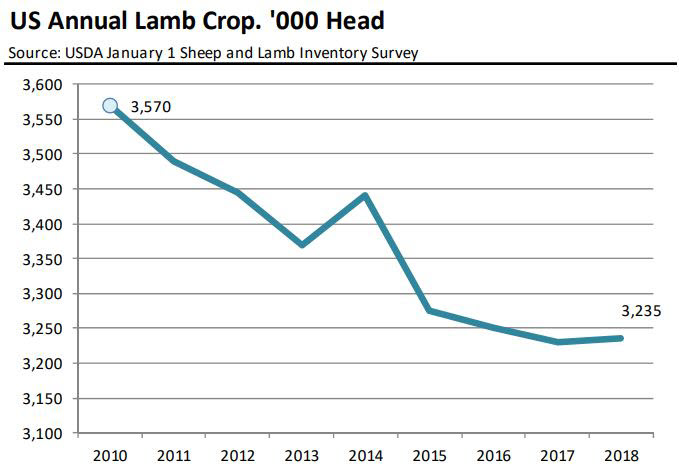

The 2018 US lamb crop was estimated at 3.2 million head, which was a slight gain on the previous year due to an improvement in weaning rates. In 2019, growth in the lamb crop is not expected given the decline in breeding numbers.

With producers retaining fewer lambs for breeder replacements, more stock is available for market. The total inventory of market lambs at the start of 2019 was 1.3 million head, 0.6% higher year-on-year.

Imported lamb market

Imports from both Australia and New Zealand have continued at high volumes in 2019, benefiting from high US prices and a strong US dollar. For the year so far (through 2 March), Australian lamb imports totalled 12,041 tonnes shipped weight, up 21% on the previous year.

Prices have held firm despite increased supply. The price of chilled Australian racks are up 10-15% year-on-year (depending on size), while most other cuts are up from 1-10%.

Read the latest monthly US Lamb Market Update prepared by Steiner Consulting