Rain restores hope in cattle market

On the back of useful rainfall in some key supply regions, increased restocker competition saw the Eastern Young Cattle Indicator (EYCI) reverse its sharp downward trend.

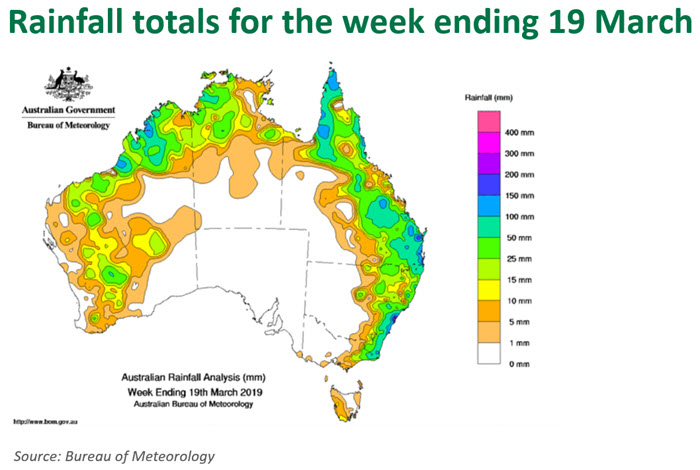

Despite a clear need for follow-up falls, weekend rainfall saw a noticeable shift in market sentiment. Yardings fell significantly over the past fortnight, with processor and feeder buyers competing for reduced supply. Tentative restocker interest was also observed in some markets.

Prices

On Tuesday, 19 March, the EYCI averaged 421¢/kg carcase weight (cwt), up 36¢ week-on-week. Tuesday’s 6% daily rise represents the largest day-on-day gain the indicator has ever recorded, with lower volumes and increased restocker competition both factors.

Notably, the number of EYCI eligible cattle (on which the indicator is based) moving through saleyards has fallen considerably in recent weeks. For the week ending 19 March, 8,777 head contributed to the EYCI, compared to 19,106 for the week ending 7 March. The change in volume goes some way to explaining current market volatility.

Turning to other indicators, cows were the star performers, with the eastern states medium cow indicator rising 14% week-on-week, to average 152¢/kg live weight (lwt). Heavy steers were more subdued, rising 8% to 267¢/kg lwt, while feeder steers rose 6% to 248¢/kg lwt.

Looking forward, young cattle and breeding stock are more likely to see the strongest price gains in the event of improved conditions. Currently, the EYCI and medium cow indicators are down 25% and 29% year-on-year, respectively.

Medium and heavy steers sit 1% and 6% below year-ago levels, respectively. Finished cattle are likely to see less volatility than the store market in the coming months, with prices supported by diminished supply and strong international demand.

Queensland

Rain brought a renewed sense of hope across south-east Queensland, with some areas receiving their first falls since December. Some notable weekly totals (rounded) include Toowoomba (80mm), Springsure (80mm), Miles (75mm), Emerald (75mm), Warwick (75mm) and Dalby (45mm). Falls decreased further to the west, with Roma receiving 25mm.

Over the past fortnight, throughput in National Livestock Reporting Service (NLRS) reported Queensland saleyards fell 57%, totalling 12,000 head for the week ending 19 March. The Dalby and Roma sales had a strong influence on the EYCI, with the reduced stock traded selling to dearer trends.

Overall, EYCI eligible cattle remain discounted in Queensland relative to southern states, averaging 410¢/kg cwt, compared to 431¢/kg cwt in NSW and 465¢/kg cwt in Victoria.

NSW

Apart from the areas in the northeast corner of the state and southern coastal regions, rainfall was more restricted across NSW. Despite the limited nature of the rain, market trends were comparable to those in Queensland, with reduced yardings, renewed restocker interest and rising prices apparent in most yards.

Yardings in NSW fell 48% over a two-week period, totalling 19,000 head for the week ending 19 March. Numbers fell considerably in Tamworth, Dubbo and Gunnedah on the back of an extended period of heightened yardings. Prices were stronger across most categories, albeit off reduced numbers.