Season to drive feeder market

Price trends for feeder cattle are typically driven by seasonal supply, however 2016 saw this trend shift as competition from restockers ramped up, pushing the market to new highs. Historically when restocker demand has become influential in the market, and the cattle herd is rebuilding, feeder cattle prices have varied from the norm – so what may be expected for 2017?

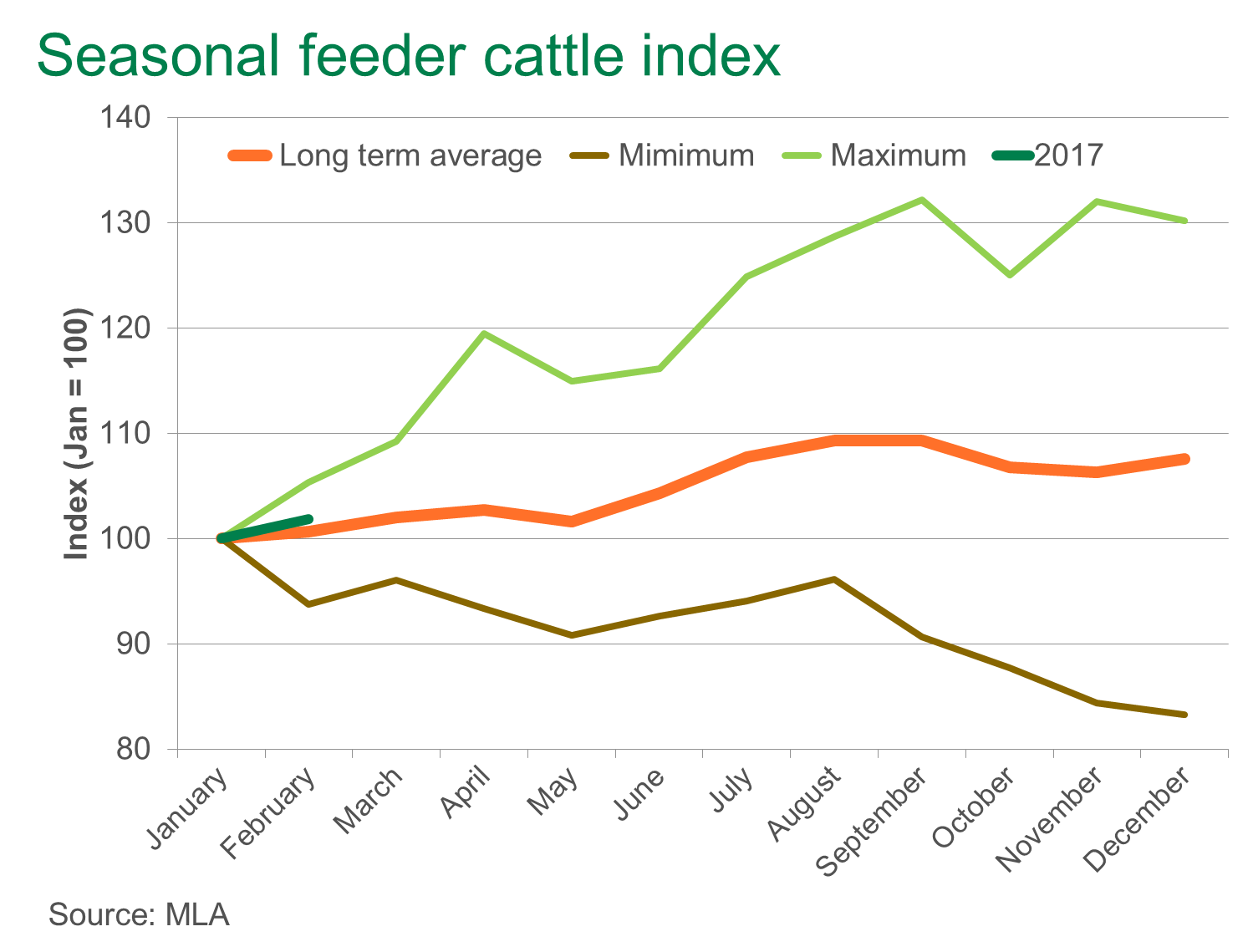

Throughout most years, troughs in feeder cattle prices occur during May, as more young cattle enter the market, and again during October and November. Meanwhile, prices usually rally (in a strong year) or recover somewhat (in a weaker year) over the winter months. As illustrated in the graph below, this seasonal trend is true of the long term average (2008-2015) and in both the strongest and weakest market trends (since 2008). 2017 thus far is tracking similar to that of the average. The remainder of the year will be determined by the season – the Bureau of Meteorology three month outlook has most of the eastern states forecast to receive below average rainfall – and the appetite of restockers in the market.

Providing more clues to how feeder prices might perform for the rest of 2017 are the trends that were observed as the herd recovered during 2010. Restocker demand lifted throughout the year and into 2011, on the back of excellent seasonal conditions and tight supplies, resulting in feeder cattle prices finishing 2010 more than 20% higher from the January average. 2016 also peaked more than 20% above where it averaged in January, however eased toward the end of the year as supplies lifted following a dry November and poorer seasonal outlook.

In years where poor seasonal conditions have prevailed and resulted in greater turnoff, such as 2009 and 2013, seasonal price troughs in the feeder cattle market have been exacerbated – with prices declining up to 8% during the autumn trough and 2% during the spring trough (following the winter rally) from where the year began.

Going forward, seasonal conditions throughout 2017 will dictate market dynamics, particularly restocker demand and the availability of young cattle. However, supplies are still anticipated to remain tight, with the herd estimated to be at a 20-year low, continuing to support the market.