Subscribe to The Weekly e-newsletter

For in-depth red meat market news, information and analysis.

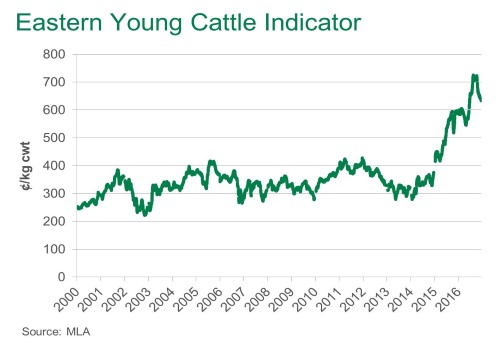

Seasonal decline, or start of a correction?

15 December 2016

As cattle sales start drawing to a close for another year, the market has followed what seems to be a typical seasonal spring decline.

In fact, the Eastern Young Cattle Indicator (EYCI) declined 10% from September to December, which compared to other years is very close to the seasonal pattern (7% was the average decline from 2005-2012). At the same time, and causing the decline, was the corresponding rise in the number of cattle on the market – albeit, not to the same extent as the previous two years. Eastern states weekly cattle slaughter increased 19% over the period, while saleyard throughput increased 64%, averaging 62,000 head for the first two weeks of December.

So the question is, will the downward price trajectory continue, or will the market turnaround in the early stages of 2017?

In the past, the cattle indicators have increased by an average 2% from January through to March, reflecting the general contraction in cattle availability. Considering the early stages of herd rebuilding are evident, and considering the significant rise in cattle on the market in the final quarter of 2016, the same supply pattern will more than likely follow again in 2017.

The two factors at play that will more than likely constrain the price potential for this period are competition for finished cattle, and restocker demand. Restockers specifically have shown considerable intent over the past eight months to replenish depleted herds, and with the likelihood of a hot and dry three months ahead, according to the Australian Bureau of Meteorology, this will probably cool the competition on that front.

For finished cattle prices, the Queensland over-the-hook indicators have dropped to a similar degree as young cattle prices, yet while restockers may be competing a little less fiercely, the competition between processors for the limited pool of cattle will continue to be of assistance to the market.

In short, the young cattle market could be impacted by the summer heat, while the demand for finished cattle in the first quarter of 2017 is likely to remain strong. Beyond this period though and as is often the case, whether or not the recent decline is simply seasonal or a correction will be heavily influenced by the weather. A prolonged bout of dry conditions will more than likely result in a market correction, or falls greater than what would normally occur through seasonal patterns.

The EYCI finished 2016 at 634.5¢/kg cwt, up 47.5¢ from the same time last year.