How seasonal conditions are impacting the cattle market

Key points

-

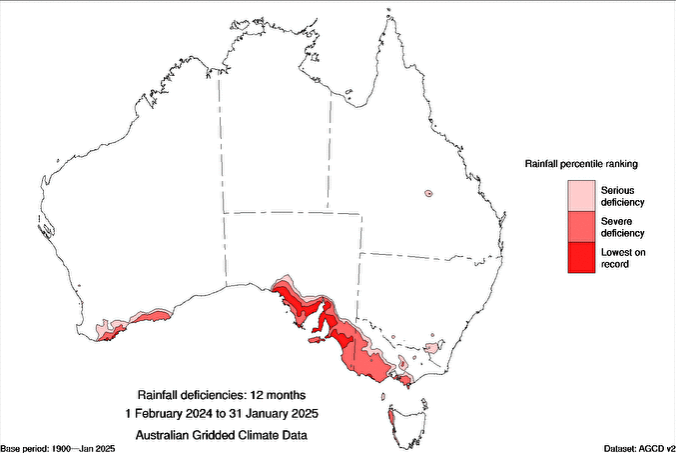

The dry weather across southern Australia is impacting current cattle market conditions.

-

Finished cattle prices are highest in Victoria and SA due to lower supply of suitable cattle in the region.

-

Heavy steer prices are higher than restocker prices in Victoria and SA, allowing traders to capitalise on price rises and weight gain.

Some regions in southern Australia – mainly south-east Victoria and south-west SA – are in the grips of a bad drought (the worst since 1967 in many areas).

Meanwhile, the northern wet season arrived late this year, with many areas recorded a drier-than-usual January. Despite this, only a small area of Queensland around Barcaldine is declared “in drought” according to the Bureau of Meteorology (BOM).

These seasonal conditions are having a profound impact on the market.

Caption: Rainfall deficiencies from 1 February 2024 – 31 January 2025 Source: Bureau of Meteorology.

Premium in the south, discount in the north

On 11 February 2024, the differential between the National Young Cattle Indicator (NYCI) and the National Heavy Steer Indicator was 50¢/kg liveweight (lwt). Now, the difference between the NYCI and Heavy Steer Indicator has closed to 11¢/kg lwt. During both November and December 2024, the Heavy Steer price exceeded that of the restocker animals included in the NYCI.

However, these dynamics are not uniform nationwide.

In Roma, the Heavy Steer Indicator is currently trading at a 25¢/kg lwt discount to the Young Restocker. In this scenario, a trader relies on weight gain to return a trading profit.

In the southern markets, using Leongatha as an example, the Heavy Steer price is commanding a 76¢/kg premium to restocker prices.

Southern yards now the highest paid

The highest prices for heavy steers (finished animals bought by processors) are all recorded at saleyards in either Victoria or SA, namely: Leongatha (378¢/kg), Echuca (351¢/kg), Wodonga (346¢/kg), Shepparton (344¢/kg) and Mt Gambier (343¢/kg).

A year ago, saleyards in the north of the country held three of the top five prices for heavy steers, including Warwick, Dalby and Casino.

Over the same period, the throughput of heavy steers in the five Victorian/SA yards listed above (Leongatha/Packenham, Echuca, Wodonga, Shepparton and Mt Gambier) have fallen 47% due to dry conditions affecting the supply and quality of finished cattle.

This climate-driven reduction in supply has increased prices.

What does this mean for producers and traders?

The closing price differential between the NYCI and Heavy Steer Indicator makes trading steers generally attractive at present. It reflects that the market for restockers has softened as the northern herd rebuild plateaus and the south enters a destock.

It could also indicate that buyers in the south expect supply to get lean as the year progresses, with dry conditions forecast to continue.

For producers, the margins on trades may have improved as the premium paid for inbound animals has closed and producers can just focus on adding kilos of weight – rather than also having to recoup the young animals’ purchase costs. This is especially true for southern traders, with access to pasture they are currently able to boost returns through both weight gain and the price premium for heavy cattle. Those in the north are still only relying solely on weight gain.

Attribute content to: Stephen Bignell, MLA Manager – Market Information